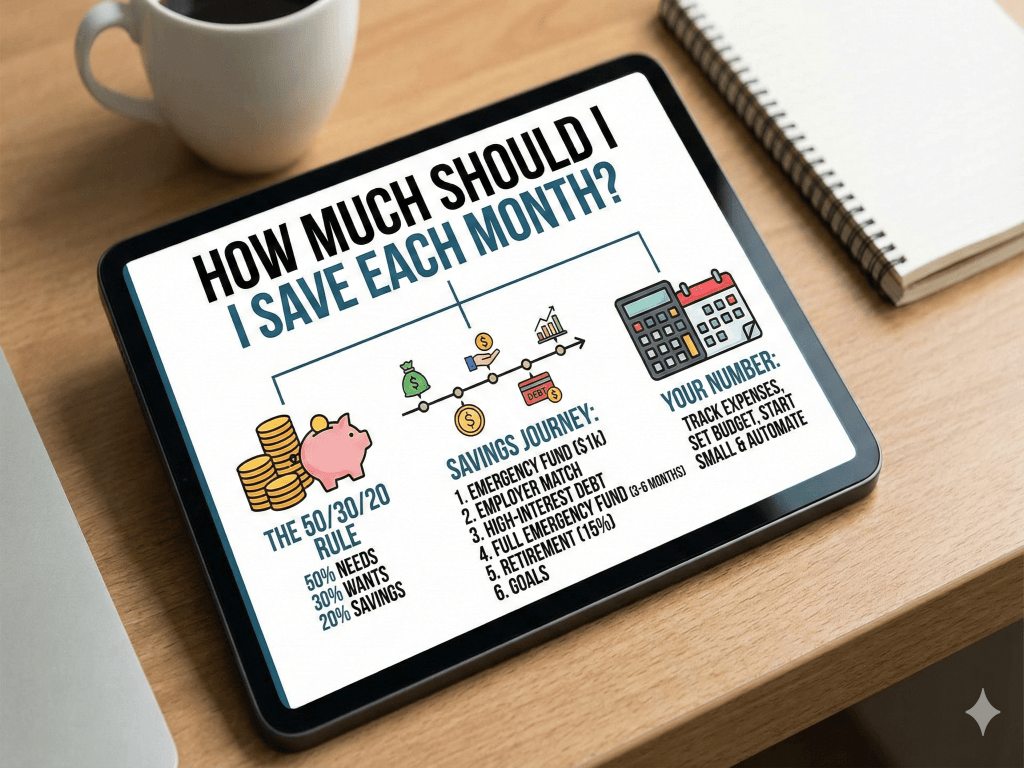

1. “How much should I save each month?”

There’s no magic number, but the most effective starting point is the 50/30/20 rule:

- 50% needs

- 30% wants

- 20% savings/debt payoff

If 20% feels too high, simply begin with €50–€100 monthly and automate it. Slowly increase it each time your income rises. Consistency builds wealth far more than perfection.

2. “Do I need an emergency fund?”

Yes — it’s your financial safety net. Aim for 3–6 months of essential expenses.

Start small: even €500–€1,000 creates breathing room. Store it in a high-yield savings account, not in investments where the value might drop.

3. “Should I pay off debt first or invest first?”

If the interest rate on your debt is above 7%, pay it off first — guaranteed returns beat market uncertainty.

If it’s lower, you can safely split: for example, 70% toward debt, 30% toward investing, so you keep building wealth while reducing liabilities.

4. “How do I start investing if I’m a beginner?”

Keep it simple:

- Open a brokerage account.

- Start with broad index funds or ETFs (example: S&P 500 ETF + global diversification).

- Invest a fixed amount every month.

Avoid stock-picking early on. Time in the market beats timing the market.

5. “How can I improve my credit score?”

Three habits make the biggest difference:

- Pay every bill on time.

- Keep credit utilization below 30%.

- Avoid opening too many accounts at once.

A bonus tip: request a credit limit increase every 6–12 months to automatically improve utilization.

6. “What’s the best way to budget without feeling restricted?”

Use a “pay yourself first” budget: automate savings and bill payments, then spend the rest guilt-free.

This approach works because it focuses on your priorities before lifestyle expenses — not after.

7. “How much should I have saved for retirement?”

A widely used guideline is the 25× rule:

Estimate your needed annual retirement income and multiply by 25.

Example: Want €30,000 per year in retirement?

You’ll need about €750,000 invested.

But even small, early contributions add up thanks to compound growth — start now, even with €20 per week.

8. “Is renting a waste of money?”

Not necessarily. Renting offers flexibility, lower upfront costs, and no maintenance expenses.

Buying makes sense when:

- You plan to stay 7+ years,

- Mortgage + taxes + maintenance are affordable,

- And you have a solid emergency fund.

It’s less about status — more about long-term financial fit.

9. “How can I increase my income without switching careers?”

Focus on skill stacking, not radical career changes.

Ways to boost income:

- Freelance your existing skills

- Ask for a raise with quantified results

- Build micro-skills (automation, data handling, AI tools)

- Monetize hobbies via digital products or services

Small skill upgrades often lead to the biggest income jumps.

10. “How do I prevent overspending?”

Overspending usually comes from frictionless spending.

Try these tactics:

- Set a 24-hour rule before buying non-essentials

- Delete saved cards from shopping apps

- Use a separate “fun money” account

- Track only your bad habits, not your whole budget

The goal isn’t to remove joy — it’s to make buying more intentional.