Take control of your financial future without the complexity.

In a world of intricate financial advice, the 50/30/20 budget stands out for its stunning simplicity and powerful effectiveness. If you feel overwhelmed by spreadsheets or tracking every penny, this method offers a breath of fresh air.

This isn’t just another article explaining the same old percentages. We’re diving deeper to give you a unique, actionable guide on how to truly make the 50/30/20 rule work for your real life, helping you build a sustainable path to financial wellness.

What is the 50/30/20 Budget Rule? Beyond the Basic Percentages

At its core, the 50/30/20 rule is a percentage-based framework for organizing your monthly after-tax income. The concept is simple:

- 50% for Needs: Half of your income is allocated to essential expenses you cannot avoid.

- 30% for Wants: Thirty percent is for non-essential, lifestyle choices that bring you joy.

- 20% for Savings & Debt Repayment: A full fifth of your income is dedicated to securing your financial future.

The unique power of this budget lies in its mindset. It doesn’t ask you to cut out all fun or live a life of deprivation. Instead, it encourages balance, ensuring you cover your essentials, enjoy your life today, and simultaneously build a safer tomorrow. It’s a plan for your money that grows and adapts with you.

Your First Step: Finding Your “Take-Home” Number

Before you can divide anything, you need the right number. For the 50/30/20 rule, you always start with your net income. This is the money that actually lands in your bank account after taxes, health insurance premiums, and other mandatory deductions are taken out.

If your employer automatically deducts retirement contributions, different sources suggest different approaches. Some recommend adding that contribution back into your net income for this calculation, as it technically falls under “savings”. The most important thing is to be consistent with whichever method you choose.

Plug in your income, and let our calculator break it down instantly. Start balancing your spending and saving smarter today! ????✨

A Modern Look at the Three Categories

Understanding these categories is key, but the lines can sometimes blur. Let’s clarify them with a contemporary perspective.

1. Needs (50%): The Non-Negotiables

Needs are expenses fundamental to your survival and basic obligations. A good test is to ask, “Could I live without this?” If the answer is no, it’s likely a need.

Traditional Examples:

- Rent or Mortgage

- Utilities (electricity, water, gas)

- Basic Groceries

- Health Insurance and Essential Medical Care

- Transportation (car payment, gas, public transit fare)

- Minimum Required Payments on Debts (credit cards, student loans)

The Gray Area & Modern Take:

- Internet & Phone: In today’s connected world, these are often essential for work and communication. They are likely a “need,” but the latest iPhone upgrade would be a “want.”

- Childcare: For working parents, this is an undeniable necessity.

- Basic Clothing: Think replacement socks or a warm winter coat. Designer items or fast-fashion hauls are not.

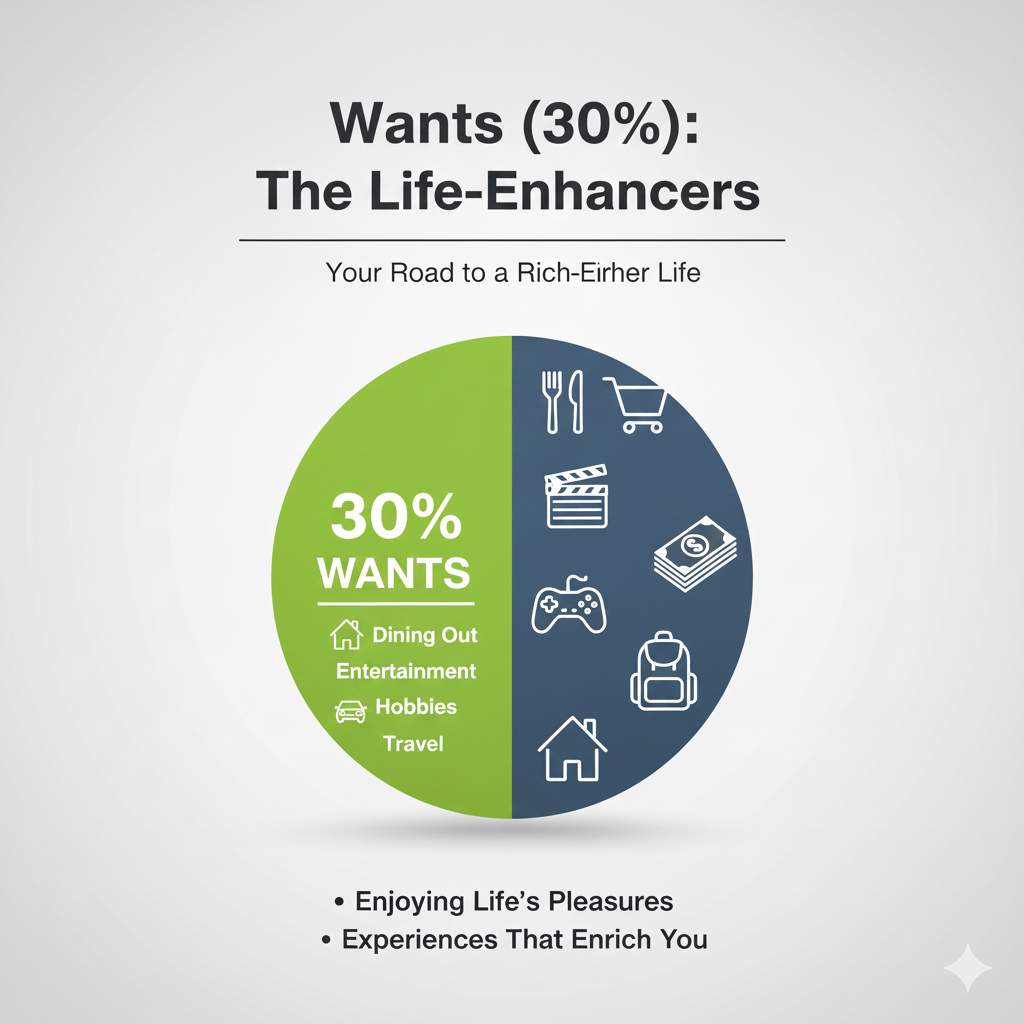

2. Wants (30%): The Life-Enhancers

This is your guilt-free zone for the things that make life enjoyable. They are discretionary and entirely optional.

Traditional Examples:

- Dining Out & Takeout Coffee

- Subscription Services (Netflix, Spotify)

- Gym Memberships (unless prescribed for health reasons)

- Vacations & Hobbies

- Concert Tickets and Entertainment

The Mindset Shift:

The unique perspective here is to see this category not as “slush funds” but as “conscious choice funds.” You are choosing to allocate resources to these items because they add value to your life. This reframe empowers you to cut back without feeling deprived when you need to shift more money to savings or debts.

3. Savings & Debt Repayment (20%): Your Future Self’s Paycheck

This is the category that builds wealth and financial security. It’s not just about stashing cash away.

What It Encompasses:

- Building an Emergency Fund (aim for 3-6 months of expenses)

- Retirement Contributions (to a 401(k), IRA, or other retirement account)

- Investing (in stocks, bonds, or mutual funds)

- Saving for Specific Goals (a home down payment, a new car, education)

- Extra Debt Payments (any payment beyond the minimum required amount)

A Key Distinction: Note that only the minimum payment on a debt is a “need.” Any extra you pay to reduce the principal faster is a “savings” activity, as it improves your long-term financial health.

Putting It Into Practice: A Unique, Actionable Plan

Let’s move beyond theory. Here is a step-by-step guide to launching your 50/30/20 budget.

Step 1: The Deep Dive & Triage

For one month, track every single expense without judgment. Use an app, a spreadsheet, or a notebook. At the end of the month, categorize each expense as a Need, Want, or Savings/Debt payment. This gives you your baseline.

Step 2: The Reality Check & Adjustment

Compare your actual spending to the 50/30/20 targets. Are your “Needs” at 60%? Are your “Savings” at 5%? Don’t panic. This is the most crucial step. The 50/30/20 rule is a guide, not a tyrant.

- If Needs > 50%: Look for ways to reduce fixed costs. Can you refinance a loan? Downgrade your phone plan? Meal prep more to lower grocery bills? If you live in a high-cost area, you may need to adjust the percentages to be more realistic for your situation, like a 60/25/15 split.

- If Savings < 20%: This is where you use your “Wants” as a lever. Scrutinize your discretionary spending. Identify subscriptions you don’t use, or commit to eating out one less time per week. Redirect every found dollar here.

Step 3: Automate & Optimize

Make your budget fail-proof. Set up automatic transfers so that on payday, 20% of your income is immediately moved to a savings or investment account. This follows the “Pay Yourself First” philosophy and ensures your future is funded before you even see the money.

The table below provides a quick-glance summary of the rule and its categories:

| Category | Ideal Allocation | Core Purpose | Key Questions to Ask |

|---|---|---|---|

| Needs | 50% | Cover essential living expenses & minimum debt payments | “Is this mandatory for my health, work, or basic living?” |

| Wants | 30% | Fund lifestyle choices & personal enjoyment | “Does this bring me joy or value? Is it a choice, not a necessity?” |

| Savings & Debt | 20% | Build financial security & reduce high-interest debt | “Is this improving my long-term financial health?” |

When the 50/30/20 Rule Needs a Personal Tweak

This rule is brilliant, but it’s not one-size-fits-all. Its true strength is its flexibility.

- For High-Cost City Dwellers: If you live in a major metropolitan area like San Francisco or New York, keeping “Needs” at 50% can be nearly impossible. Be honest with yourself and adjust the percentages. The principle of balancing present needs with future security is what matters most.

- For the Debt-Heavy: If you have high-interest debt, consider a temporary aggressive shift. You might use a 70/20/10 model (70% Needs, 20% Extra Debt, 10% Wants) to crush your debt faster, then return to the standard model.

- For High-Earners with Fewer Needs: You might find your “Needs” are only 40%. Fantastic! You can choose to funnel the extra 10% into savings or allow yourself more “Wants.” The choice is yours.

Beyond the 50/30/20: Other Budgeting Strategies

If you try the 50/30/20 and it doesn’t resonate, other methods might be a better fit:

- Zero-Based Budgeting: Every dollar of your income is assigned a job, leaving you with zero unallocated money. Excellent for meticulous tracking.

- The Envelope System: Use physical or digital “envelopes” for spending categories. When the envelope is empty, you stop spending in that category. Great for controlling discretionary spending.

- The 80/20 Plan: A simplified version where you automatically save 20% of your income and freely spend the remaining 80%.

Your Financial Journey Starts Now

The 50/30/20 budgeting rule is more than a math formula; it’s a philosophy for making intentional choices with your money. It gives you permission to spend on today’s joys while systematically building for tomorrow’s security.

Don’t strive for perfection. The goal is progress. Start today by calculating your net income and doing a quick category audit. Your future, financially secure self will thank you for taking this first, powerful step.

Are you ready to give the 50/30/20 budget a try? Share which category you find the most challenging to balance in the comments below!